a:8:{s:8:”location”;a:1:{i:0;a:1:{i:0;a:3:{s:5:”param”;s:12:”options_page”;s:8:”operator”;s:2:”==”;s:5:”value”;s:22:”theme-general-settings”;}}}s:8:”position”;s:6:”normal”;s:5:”style”;s:7:”default”;s:15:”label_placement”;s:3:”top”;s:21:”instruction_placement”;s:5:”label”;s:14:”hide_on_screen”;s:0:””;s:11:”description”;s:0:””;s:12:”show_in_rest”;i:0;}

Blog and News Content

a:8:{s:8:”location”;a:1:{i:0;a:1:{i:0;a:3:{s:5:”param”;s:13:”page_template”;s:8:”operator”;s:2:”==”;s:5:”value”;s:25:”page-flexible-content.php”;}}}s:8:”position”;s:6:”normal”;s:5:”style”;s:7:”default”;s:15:”label_placement”;s:3:”top”;s:21:”instruction_placement”;s:5:”label”;s:14:”hide_on_screen”;s:0:””;s:11:”description”;s:0:””;s:12:”show_in_rest”;i:0;}

a:8:{s:8:”location”;a:1:{i:0;a:1:{i:0;a:3:{s:5:”param”;s:9:”post_type”;s:8:”operator”;s:2:”==”;s:5:”value”;s:11:”testimonial”;}}}s:8:”position”;s:6:”normal”;s:5:”style”;s:7:”default”;s:15:”label_placement”;s:3:”top”;s:21:”instruction_placement”;s:5:”label”;s:14:”hide_on_screen”;s:0:””;s:11:”description”;s:0:””;s:12:”show_in_rest”;i:0;}

As a business owner, it is important to examine potential commercial risks and implement strategies to deal with them. One efficient approach is purchasing insurance. However, for some businesses, traditional insurance is too expensive or generally incapable of meeting their needs. As a result, self-insurance has become an attractive alternative.

But what is self-insurance all about? How does it even work? Are there specific types of coverages for self-insured businesses? How can you manage your claims effectively? This self-insurance guide addresses all these concerns.

What Is Self-Insurance?

Self-insurance is an alternative to purchasing traditional, “dollar one” insurance, where businesses set aside money to pay for possible losses. As opposed to traditional insurance, which involves a third-party insurance provider, the business incurs the costs for accidents, medical bills, thefts, lawsuits and so on from their own pockets.

There are many reasons for self-insuring your business. For example, you can save money you would otherwise spend on insurance premiums and invest it in other parts of your business. It allows you to set money aside to cater to perils as they arise, thereby preventing overpayment. Additionally, depending on how you manage the savings, it can yield interest, especially when you have infrequent losses. Self-insurance also gives you tailored coverage since you can create an insurance plan that favors your business needs.

While enjoying all these benefits, self-insured businesses must comply with all relevant federal and state insurance regulations. For example, although business owners have the freedom to plan their insurance, certain coverages like workers’ compensation, unemployment and disability insurance are mandatory.

One significant challenge self-insurers face is claims management, especially when there are large volumes of data. The good news is that you can use advanced cloud-based tools to simplify your claims management. Incident-based cloud management technology facilitates data-driven insights, provides audit capabilities and custom reporting and generally streamlines every aspect of self-insurance claims management.

How Does Self-Insurance Work?

Self-insured businesses assess potential risks and set aside money to cover expenses, if those events occur. When someone files a claim, the company pays directly from its own funds. The employer may create a dedicated team to monitor and process claims or hire the services of a third-party administrator (TPA) to handle all things claims related. Alternatively, the business can manage some parts of the self-insurance program and reserve other functions for a TPA.

The dedicated staff or TPA will calculate the amount to set aside, considering your insurance needs, potential risks, and the expected claims that could arise. Anticipating these challenges and potential costs will determine your risk tolerance.

For example, if your business has a high chance of encountering lawsuits — as in the case of product defects, professional liability or personal injuries — you will set aside money for indemnity settlements plus expenses like attorney fees and court expenses. If your business collects, stores and uses large volumes of customer data, reserving money for potential data breaches and the costs to resolve them will be required.

After weighing out the possibilities of losses, the business will determine what its self-insured retention (SIR) should be. Although a business is “self-insured,” it is unlikely to be self-insured to unlimited liability. The self-insured retention is the amount of money a business covers itself, before the excess / stop-loss coverage kicks in. Limits are typically set on a per-occurrence basis and on an aggregate basis. The higher the retention, the lower the insurance premiums will be, but the more risk the business bears in the event of a loss. Once the self-insured retention limits are reached, an insurance carrier will cover costs, limiting liability to the business.

Whether you develop an internal self-insurance team, partner with a TPA or leverage the advantages of both, using a cloud management software to manage claims within the self-insured retention is recommended. An incident-based self-insurance claims management technology combines data from internal and external sources in a system, giving you a single source of truth.

What Does Self-Insurance Cover?

Four common self-insurance coverages for businesses are

- General liability insurance: Business or general liability insurance covers claims during normal business operations, like slips and falls and property damage. The coverage may change depending on the nature of the business you operate.

- Property insurance: Self-insured businesses may set aside money for damages to commercial assets, like buildings, inventory and equipment. Potential risks include theft, fire and flood damage.

- Auto insurance: Auto or vehicle insurance is necessary for businesses that own commercial vehicles, like vans and trucks. The coverage may pay for property damage and injuries if an employee causes an accident.

- Workers’ compensation insurance: Insurance covering job-related injuries to employees. Rules vary significantly by state.

How Is Self-Insurance Different From Traditional Insurance?

The obvious difference between self-insurance and traditional insurance is the absence of a third-party provider. This means, for all claims up to your self-insured limit, you need to do everything the third-party insurance provider would do yourself or with the assistance of a TPA. Instead of purchasing full coverage from an insurance company, the business saves cash and creates a reserve for covering potential losses. The business owner uses an internal insurance team or TPA to determine how much would be enough to cover the losses. For example, in the case of workers’ compensation, the company acts as the employer and insurance provider to the employees and generally bears the potential liabilities that would otherwise be covered by an insurance carrier.

Are There Any Requirements for Self-Insurance?

Self-insured businesses should meet the following requirements:

- Legal compliance: The company must comply with all relevant insurance laws and regulations, considering the mandatory coverages.

- Financial stability: Self-insured businesses should be financially stable and capable of covering expenses that arise.

- Risk assessment: The employer should have a team for comprehensive risk assessments and mitigation.

- Administration: It is best to have claims management systems to streamline insurance administration.

The specific requirements will vary by state and by the type of coverage being self-insured. Workers’ compensation has far more regulatory requirements than property insurance. Therefore, it is common for business to self-insure certain types of losses (e.g. property) and maintain traditional insurance for others (e.g. workers’ compensation).

How Do You Become Self-Insured?

Here are five ways you can manage self-insurance:

1. Create a Strong Team

Whether you establish an internal insurance and risk assessment team or choose a TPA, ensure the team is well-positioned to provide the required service. The insurance professionals should understand your business needs and offer clear plans to deliver results. Additionally, the team should ensure compliance with federal and state laws.

2. Do a Comprehensive Cash Flow Analysis

Self-insurance is only possible if you have sufficient funds to cover losses. Therefore, it’s vital to do a comprehensive financial analysis to understand your financial situation and insurance needs. This would help you determine how much loss you can cover and set limits that don’t endanger the health of the business.

3. Develop a Self-Insurance Policy

Develop a policy or guideline that covers eligibility, exclusions, benefit coverages, policy limits, and cost-sharing. Weigh the advantages of the self-insured plan, such as the lower cost coverage and flexibility against administrative responsibilities and increased risks. This will help you know whether the plan is effective and worth pursuing.

4. Get Stop-Loss Insurance Coverage

Stop-loss insurance is the coverage that reimburses self-insured businesses for high claims or those that exceed the self-insured retention’s limits. The employer sets a claim limit, above which the claims carrier will cater to the difference. It is like insuring your insurance. The arrangement helps businesses address unexpected risks.

5. Use Claims Management Software

Incident-based claims management solutions designed for self-insured businesses have many benefits. They enable you to learn from every incident and identify the root cause of accidents. That way, you can adequately assess the risks and implement strategies to reduce them. Leveraging these advanced solutions saves money and ensures you are maximizing savings for your self-insured program.

APP Tech — Claims Management Software for Self-Insured Businesses

Self-insured businesses assume the company’s potential risks instead of relying on third-party insurers for coverage. This saves money and allows the business to create a tailored plan according to its needs. While managing self-insured companies can be complex, cloud management software makes claims processing simple and efficient.

APP Tech’s Cloud Claims is an advanced incident-based system that provides end-to-end cloud solutions for your claims management. It enables you to analyze losses, track claims and policies, and track all your finances. Cloud Claims is also customizable. If you want to learn more about how to streamline your claims management processes, contact us now!

Discover the various claim management trends from the field that self-insured businesses, third-party administrators (TPAs) and insurance solution providers must know. Staying up-to-date with the current trends in claim management will position your organization for success. In 2023, as claims processing continues evolving, we unveil the pivotal claims processing trends that will shape your strategies.

From streamlining operations to harnessing advanced technologies, this guide will list and explain the top trends in claim processing in 2023 that shape efficient and forward-thinking claim management practices.

Claim Management Trends in 2023

Let’s dive into current trends in claim management and explore the transformative claims processing trends driving innovation and efficiency.

1. Incident-Based Approach — Redefining Claims Management

Amid claim management trends in 2023, one trend stands out — the incident-based approach. Departing from traditional methods, this approach revolves around real-time incident reporting. By promptly ingesting data for informed decision-making, businesses ensure accuracy and relevance.

Cloud Claims, a sophisticated solution for incident-based processing, bolstered this transition. With the ability to swiftly report incidents through smartphones, complete with attached visuals, Cloud Claims pioneers a seamless shift toward efficiency and precision. As businesses embrace this trend, they redefine their claim management landscape, setting the stage for enhanced operational agility and optimal outcomes.

2. Expedited Data Ingestion and Prompt Decision-Making

Timely and accurate data is the foundation for efficient claims processing and technology plays a pivotal role. Harnessing innovative tools, stakeholders can swiftly ingest data, triggering real-time alerts that keep all parties informed. This accelerated flow enables agile decision-making, transforming claims into actionable insights.

By adopting configurable systems tailored to individual client needs, businesses cultivate an environment where prompt, well-informed decisions become the norm. In the claims industry, the ability to expedite data flows and facilitate rapid decisions propels organizations toward operational excellence and heightened stakeholder satisfaction.

3. Configurable Systems — Adapting to Unique Client Needs

In 2023, claim management is shifting toward adaptable and client-centric systems. Every organization operates with its distinct processes, workflows and requirements. Configurable systems offer the flexibility to mold claim management tools according to these individual needs. This trend ensures that businesses no longer conform to rigid, pre-set structures but can instead design seamless workflows that align with their operations.

Cloud Claims offers a purpose-built incident-based claims management system tailored to the intricate demands of self-insured entities, TPAs and insurance providers. This adaptable approach streamlines claims processing and maximizes efficiency, accuracy and client satisfaction. As the industry utilizes this trend, businesses can expect enhanced control, improved outcomes and a competitive edge in claim management.

4. Bridging the Gap — Self-Insured Corporates and Big Insurers

Self-insured entities are no longer confined to antiquated systems or limited by technological constraints. This trend acknowledges the importance of equipping self-insured corporates with the same advanced claims processing capabilities that big insurers have long enjoyed. Cloud Claims plays a pivotal role by offering purpose-built technology tailored to the unique needs of self-insured businesses.

By adopting this trend, organizations can surpass the limitations of email chains, spreadsheets and outdated systems. Cloud Claims empowers self-insured corporates to harness efficient claims handling, data-driven insights and streamlined processes like those of established insurers. This trend ensures that self-insured entities can compete on a level playing field, achieve substantial cost savings and optimize their claims management practices for success.

5. Real-Time Insight and Stakeholder Participation

Looking further into claim management trends, real-time insight and stakeholder participation emerge as central catalysts of efficient and proactive claims processing. This trend redefines the role of corporate stakeholders, enabling them to actively improve safety and reduce loss.

Cloud Claims enable real-time insights, providing stakeholders with a comprehensive view of organizational activities. Stakeholders can make informed decisions, monitor trends and contribute to risk mitigation strategies by actively participating in the claims management process. Real-time insight and stakeholder participation enhance claims processing and foster collaboration, transparency and accountability.

Trusting APP Tech for Incident-Based Claim Management

When it comes to claim management trends, staying ahead is crucial. As insurance solution providers seek effective strategies for 2023, key claim management trends shape these strategies and facilitate informed decision-making. The incident-based approach innovates claims management, while real-time insights and configurable systems expedite decisions.

APP Tech’s Cloud Claims seamlessly blends cutting-edge features with a user-friendly design. By bridging the gap between self-insured corporates and industry giants, Cloud Claims ensures efficient claims processing akin to big insurers. As you navigate these current trends in claim management, remember — Cloud Claims is not just software, it is a partner in simplifying complexity.

Request a Demo today and learn more about incident-based claim management.

As a business exploring avenues to optimize risk management, the concept of self-insurance presents a compelling opportunity. Self-insurance can result in greater control of your claims and cost savings, but this comes with additional responsibilities. In this post, we’ll review the essential considerations for businesses contemplating self-insurance.

Among these considerations, we highlight the significance of robust claim management solutions for self-insured businesses. Discover how leveraging advanced technologies can streamline claims handling, enhance risk management and unlock the potential benefits of self-insurance tailored to your specific needs.

Should your company consider self-insurance? Let’s find out.

The Pros and Cons of Self-Insurance

When considering self-insurance, companies must carefully weigh the advantages and disadvantages. Here are the key pros and cons.

Pros of Self-Insurance

Discover the advantages that make self-insurance an enticing option for businesses:

- Cost savings and control: Self-insured companies have the potential to save on insurance premiums by eliminating the profit margin of traditional insurers. Additionally, they retain control over risk management strategies and claim payouts.

- Tailored coverage: Self-insurance allows customized insurance plans to match specific risk profiles and business needs, ensuring comprehensive coverage where it matters most.

- Investment opportunities: Instead of paying premiums to external insurers, self-insured businesses can invest these funds, potentially yielding returns that contribute to financial stability.

- Long-term stability: With stable claim experience and risk management practices, self-insurance can offer more predictable and consistent costs over time.

Cons of Self-Insurance

Carefully consider the potential drawbacks and challenges associated with self-insurance to make well-informed decisions:

- Financial exposure: Self-insured businesses are directly liable for claims, which can pose significant financial risks in case of large or catastrophic losses.

- Cash flow management: Setting aside reserves for potential claims requires effective cash flow management and financial planning.

- Regulatory compliance: Self-insured firms must comply with state regulations and requirements, necessitating diligent adherence to legal obligations.

- Administrative burden: Managing claims and risk internally demands dedicated resources and expertise, potentially increasing administrative complexities.

10 Important Business Considerations for Self-Insurance

Before deciding to go self-insured, businesses must carefully analyze critical factors that impact their risk management strategy. These considerations ensure a comprehensive evaluation of the feasibility and suitability of self-insurance for your company’s unique needs. Self-insurance is not an all-or-nothing proposition. It may make sense to self-insure certain types of losses and conventionally insure others.

1. Risk Analysis and Assessment

Conducting a thorough risk analysis and assessment is the foundational step in considering self-insurance. Businesses must identify and evaluate potential risks, assess their frequency and severity and determine the financial implications of self-insuring against these risks. Understanding the unique risk profile of your business enables informed decision-making and effective risk management strategies.

A comprehensive risk analysis will ensure that self-insurance aligns with your company’s risk tolerance and long-term financial goals — providing the groundwork for a successful self-insurance program.

2. Financial Stability and Reserves

Financial stability is paramount for businesses considering self-insurance. Adequate reserves are essential to cover potential claims and minimize financial risks. Companies must assess their cash flow capacity to set aside resources and ensure they have sufficient funds to handle unexpected losses. Understanding the balance between risk retention and financial preparedness is critical.

Establishing a well-structured reserve fund will provide the necessary safety net and financial security, enabling the self-insured company to navigate various claim scenarios and maintain smooth operations in the face of potential challenges.

3. Regulatory Compliance

Navigating the regulatory landscape is crucial when considering self-insurance. Firms must thoroughly understand their jurisdiction’s legal requirements and obligations associated with self-insurance. Compliance with state regulations, reporting mandates and financial solvency standards is essential to avoid potential penalties and legal issues.

Partnering with experts or third-party administrators can help ensure adherence to all regulatory requirements and streamline compliance. Prioritizing regulatory compliance allows businesses to confidently embrace self-insurance while maintaining a solid reputation and standing within the industry.

4. Employee Communication and Engagement

Effective employee communication and engagement are integral to the success of self-insurance. Businesses must transparently communicate the transition to self-insurance, addressing concerns and providing clear information about the benefits and impact on employees’ coverage.

Engaging employees in the process fosters a sense of ownership and responsibility, encouraging them to be more conscious of risk management practices and claim prevention. Regular communication channels and educational resources can empower employees to participate actively in the self-insurance program — ultimately contributing to a safer work environment and better overall risk management outcomes.

5. Stop-Loss Insurance

When considering self-insurance, companies should also evaluate the option of obtaining stop-loss insurance. This essential safety net protects against catastrophic or high-cost claims that exceed predetermined thresholds. By purchasing stop-loss insurance, businesses can mitigate the financial risks associated with large claims, ensuring they don’t face overwhelming financial burdens.

Evaluating different stop-loss insurance options and understanding the coverage limits is crucial to balance self-insurance and external risk protection — allowing businesses to confidently self-insure while safeguarding against extraordinary claim scenarios.

6. Data and Analytics

Data and analytics play a pivotal role in the success of self-insurance. Companies must leverage advanced technologies and data-driven insights to make informed decisions about risk management strategies. Utilizing comprehensive data analytics enables businesses to identify trends, assess claim patterns and implement proactive measures for risk prevention.

Access to real-time analytics empowers businesses to refine their self-insurance program and optimize claims management processes continuously. By prioritizing data-driven decision-making, companies can enhance overall risk management efficacy, resulting in cost savings, improved claims handling and better risk mitigation outcomes.

7. Employee Wellness and Risk Mitigation

When self-insuring worker’s compensation losses, employee wellness and risk mitigation are crucial components of a successful self-insurance program. Businesses should prioritize promoting a culture of safety and wellness to reduce the frequency of workplace incidents and claims. Implementing robust safety protocols, employee training and wellness initiatives may significantly reduce risk.

By proactively addressing employee well-being, businesses can minimize the occurrence of claims and create a safer work environment. Integrating employee wellness and risk mitigation strategies with self-insurance helps optimize the program’s overall effectiveness and enhances the company’s ability to manage risks efficiently.

8. Long-Term Commitment

Choosing self-insurance is a long-term commitment that requires careful consideration. Firms should evaluate their ability to maintain financial stability, risk management practices and employee engagement over an extended period. Self-insurance is not a short-term solution but a strategic decision with lasting implications.

Businesses must prepare to invest in ongoing risk analysis, claim management solutions for self-insured companies and employee wellness initiatives. Assessing the company’s long-term objectives and risk appetite is crucial to ensure that self-insurance aligns with the organization’s overall vision and goals for sustained success.

9. External Expertise

Seeking external expertise is invaluable for businesses considering self-insurance. Companies can collaborate with experienced consultants, insurance brokers or third-party administrators (TPAs) to navigate the complexities of self-insurance effectively. These experts can provide invaluable insights and guidance on regulatory compliance and help design tailored self-insurance programs that align with the company’s risk profile and financial goals.

Leveraging external expertise streamlines the self-insurance implementation process. It ensures businesses have access to the knowledge and resources necessary to optimize risk management strategies, claim handling and overall success in their self-insurance journey.

10. Claim Management Capability

A robust claim management solution is essential for successful self-insurance. Businesses can invest in advanced claim management solutions — like APP Tech’s Cloud Claims — to handle and process claims efficiently. These purpose-built technologies streamline incident-based claims management, automate notifications and offer user-friendly dashboards for at-a-glance views of claims.

With features like document organization, audit capabilities and custom reporting, businesses gain transparency, data-driven insights and effective risk management. This ensures businesses can confidently embrace self-insurance with comprehensive claim management support.

If managing a self-insurance program in-house isn’t feasible, contracting the services of a third-party administrator (TPA) can fill that gap. In this case, making sure the TPA has robust claim management software should be an important consideration when choosing the TPA. In cases where you are self-managing some parts of your self-insurance program but letting a TPA manage other parts, having the ability to combine data from internal and external sources in a system like Cloud Claims means you have a single source of truth for all your loss data.

Empower Your Self-Insurance Journey With APP Tech’s Cloud Claims

As you consider if your company should consider self-insurance, remember the vital considerations that guide this strategic decision. Evaluating risk analysis, financial stability, regulatory compliance and employee engagement is paramount. Additionally, for businesses considering self-insurance, navigating claim management challenges is inevitable. That’s where comprehensive claim management software for self-insured businesses becomes invaluable.

Take charge of your risk management future — schedule a tailored Demo today and experience the efficiency of Cloud Claims.

Having a comprehensive understanding of the Centers for Medicare and Medicaid Services (CMS) is crucial for stakeholders across a range of industries, from health care providers to liability and worker’s compensation insurers. Self-insured entities, third-party administrators (TPAs) and insurance solution providers need to navigate the CMS landscape to ensure compliance, streamline operations and mitigate risks.

But what is the Centers for Medicare and Medicaid Services? Simply put, CMS is the federal agency that administers the Medicare and Medicaid programs. These programs provide health care services and coverage to millions of Americans. As a result, the CMS plays a pivotal role in the United States health care system.

In this post, we’ll explore how CMS works and the different programs CMS oversees. We will also provide an introduction to the complex world of Mandatory Second Payer and MMSEA Section 111 reporting compliance.

Roles and Responsibilities of CMS

CMS plays a vital role in administering the Medicare and Medicaid programs and ensuring access to health care coverage for different populations. CMS sets guidelines and regulations to govern these programs, fostering compliance and facilitating health care services.

Regulating and overseeing health care providers participating in Medicare and Medicaid is a primary responsibility of CMS. This involves establishing standards for provider enrollment, care quality and patient safety, and conducting surveys, audits and inspections to monitor compliance.

CMS also manages payment and reimbursement systems, establishing fee schedules, rates and payment methodologies. It strives for fair and accurate payment to providers while controlling costs and preventing fraud and abuse.

To improve health care delivery, CMS implements various initiatives and programs. It promotes evidence-based guidelines, fosters innovation and incentivizes value-based care models to enhance quality.

CMS prioritizes fraud prevention and enforcement. Sophisticated data analytics, audits, investigations and enforcement actions are employed to combat fraud, waste and abuse of taxpayer funds.

CMS collaborates closely with state governments, stakeholders and industry experts. It partners with states to administer Medicaid programs and fosters information exchange and collaboration for innovation and improved health care outcomes.

By fulfilling its roles and responsibilities, CMS ensures effective administration, regulation, and oversight of Medicare and Medicaid. This empowers self-insured entities and insurance solution providers to navigate complexities while delivering high-quality care to their claimants and beneficiaries.

Understanding CMS Programs

Medicare and Medicaid are the two programs administered by CMS. Let’s explore their significance in the health care landscape.

Medicare Program

Medicare serves as a lifeline for eligible individuals, providing essential health care coverage based on specific criteria. To qualify for Medicare, individuals must generally be aged 65 or older, but it also covers certain individuals with disabilities or end-stage renal disease.

Medicare consists of different parts, each offering specific coverage and services:

- Part A: Part of traditional Medicare, Part A includes hospital insurance and covers in-patient hospital stays, hospice care, skilled nursing facility care and limited home health care services.

- Part B: Part B is also part of traditional Medicare, and includes medical insurance and covers out-patient services, including doctor visits, preventive care, certain diagnostic tests and durable medical equipment.

- Part C: Created in 1997, Part C is part of Medicare Advantage and offers an alternative to the original Medicare, providing all-in-one coverage through private insurance plans approved by Medicare. Medicare Advantage plans often include prescription drug coverage (see Part D below) and additional benefits like dental and vision care.

- Part D: Part D, added in 2003, also forms part of Medicare Advantage and provides prescription drug coverage and helps individuals pay for prescription medications, offering a range of prescription drug plans.

Medicaid Program

Medicaid serves individuals and families with limited financial resources, offering access to essential health care services. Eligibility for Medicaid is based on income and other specific criteria, which vary from state to state. The program aims to ensure that vulnerable populations, including children, pregnant women, individuals with disabilities and the elderly, have access to comprehensive health care coverage.

In recent years, Medicaid expansion has been a significant development. Under the Affordable Care Act (ACA), states have the option to expand Medicaid eligibility to cover individuals with higher income thresholds. This expansion has extended coverage to millions of additional individuals who were previously uninsured.

Medicaid provides a broad range of covered services, including, but not limited to, hospital visits, doctor appointments, preventive care, prescription medications and mental health services. The program aims to address the health care needs of low-income populations and improve their overall well-being.

Children’s Health Insurance Program (CHIP)

Medicaid Expansion CHIP, established in 1997, is designed to fill the gap for children who do not qualify for Medicaid but still lack access to affordable private health insurance. The program ensures that eligible children have access to comprehensive health care services, including doctor visits, immunizations, hospital care and prescription medications.

Eligibility for CHIP varies by state, but generally, children in families with income levels above the Medicaid threshold can qualify. CHIP provides coverage to millions of children, ensuring their well-being and providing necessary medical support.

From preventive care to specialized treatments, CHIP covers a broad range of health care services to meet the unique needs of children, promoting their healthy growth and development.

Medicare Secondary Payer (MSP)

Medicare Secondary Payer (MSP) provisions were established in 1980 to shift payment responsibility away from Medicare, in response to concerns over the long-term financial health of the Medicare program. Initially, Medicare was designed to be the primary payer for health care services for eligible individuals aged 65 and older. However, as the program evolved, policymakers recognized the need to prevent Medicare from bearing the full burden of health care costs when other coverage options were available.

MSP refers to a set of rules and provisions established by the U.S. government to determine the order of payment when an individual has health care or injury coverage from multiple sources. The primary goal of MSP is to ensure that Medicare is not the primary payer when other sources of coverage exist. Under the MSP rules, Medicare acts as the secondary payer in situations where another entity, such as an employer group health plan, workers’ compensation, or liability insurance has the primary responsibility for covering health care costs. The primary payer must fulfill its obligations before Medicare pays for any remaining expenses.

In cases where another payer may be responsible, Medicare will make payments for health care services conditionally, known as Conditional Payments. These payments must be repaid to Medicare if a settlement, judgement, or award is made to the Medicare beneficiary in compensation for the injuries.

Additionally, MSP requires claim settlements involving Medicare beneficiaries to take Medicare’s future interests into account. This is done through Medicare Set-Asides (MSAs) arrangements, which reserve funds (i.e. “set them aside”) from a settlement to be used by Medicare to cover future medical expenses.

MSP rules help prevent unnecessary expenditures and preserve Medicare’s financial resources. They require individuals and health care providers to report any other sources of coverage to Medicare, ensuring that the program does not pay for services that should be covered by another entity.

With conditional payments, set-asides, and the many other tools in Medicare’s toolbox, complying with MSP regulations can be challenging, but it is absolutely necessary to avoid penalties and reimbursement demands from Medicare. Many companies and law firms specialize in Medicare Secondary Payer compliance and can provide expert guidance.

MMSEA Section 111 Reporting Fills a Gap for CMS

Although the Medicare Secondary Payer (MSP) provisions were long-established, CMS had no easy way to know when there was another, primary payer available. CMS relied on individual Medicare beneficiaries to alert them to other payers. There was no incentive for an individual beneficiary to do this because, so long as their medical bills were paid, the Medicare beneficiary likely didn’t care how it was paid for. Moreover, in the case of claim settlements, beneficiaries would rather pocket their settlement money than set some aside for Medicare!

This created challenges for CMS in enforcing the MSP statutes. In response, Congress strengthened CMS’s hand with the introduction of MMSEA Section 111 reporting (also known as Mandatory Insurer Reporting). It was created to fill the gap in Medicare’s view, mandating insurers and self-insurers to report information to CMS about the health care coverage of, or settlements, judgments, awards, or other payments to, Medicare beneficiaries. While this reporting serves an essential purpose in facilitating Medicare coordination and compliance, it creates yet another set of compliance challenges because it shifts the burden of notifying CMS of primary payer responsibilities from the individual Medicare beneficiaries to the insurers and self-insureds.

Overall, the implementation of MMSEA Section 111 reporting strengthened the enforcement of the MSP provisions by preventing and improving the identification and recovery of improper Medicare payments. It enhanced CMS’s ability to identify situations where other entities have primary payment responsibility, ensuring that Medicare remains the secondary payer and reducing improper billing to the program.

But complying with MMSEA Section 111 reporting involves following complex technical requirements. Reporting entities must navigate the intricacies of data collection, formatting, and submission through CMS-approved reporting channels. The process demands a thorough understanding of the reporting guidelines and protocols to ensure accurate and timely submissions.

Self-insured entities and insurance carriers may encounter challenges in gathering the necessary data for reporting. This includes identifying and tracking reportable events, collecting beneficiary information, including Social Security number and medical diagnosis information, and reconciling data across multiple systems or entities.

Failure to comply with MMSEA Section 111 reporting requirements can have significant consequences. Non-compliance, including inaccurate reporting, may result in penalties, fines or even litigation.

How an MMSEA Section 111 Reporting Solution Facilitates MSP Compliance

To mitigate these compliance challenges, organizations can consider utilizing MMSEA Section 111 reporting software to simplify and streamline the reporting workflow.

Such software offers a range of features and capabilities designed specifically for compliance with CMS requirements. These solutions provide user-friendly interfaces that guide users through the data collection, formatting, and submission processes. With built in validations and checks, they help ensure the accuracy and completeness of the reports, minimizing the risk of rejections and penalties.

By streamlining the workflow, an MMSEA Section 111 reporting solution can save time and effort. These solutions automate data gathering from internal claims systems, consolidate the necessary information, and generate the required reports to CMS. This eliminates the need for manual data entry, removes the burden of maintaining audit trails, and reduces the likelihood of errors.

Although some companies create their own systems for electronic reporting to CMS, the reporting rules change regularly and keeping home grown systems up to date requires ongoing effort and resources. Therefore, ensuring compliance with CMS reporting requirements is a key aspect of MMSEA Section 111 reporting solutions. These solutions stay up to date with the latest CMS guidelines and regulations, incorporating any changes. This ensures organizations stay compliant and avoid civil money penalties (CMPs).

Lastly, the vendors who provide MMSEA Section 111 reporting solutions can provide expert support and guidance throughout the reporting journey. They offer dedicated customer support teams that are well-versed in CMS reporting requirements. These experts can assist organizations in navigating any challenges, answering questions and providing personalized guidance to ensure successful reporting to CMS.

Unlock the Power of Seamless Reporting With MIR Express™ by APP Tech

In this comprehensive guide, we’ve explored CMS and its vital role in the health care industry. CMS’s impact is far-reaching, from administering Medicare and Medicaid programs to ensuring quality care and combating fraud. Understanding the complexities of CMS programs is essential for self-insured entities to navigate the ever-evolving landscape successfully.

When it comes to MMSEA Section 111 reporting, APP Tech’s MIR Express emerges as the ideal solution. As a user-friendly, secure, and web-based system, MIR Express simplifies the mandatory insurer reporting process for non-group health plans (NGHP). EDI and API integration options eliminate redundant data entry and can fully automate sending your data to APP Tech. With continuous updates and 100 percent adherence to CMS requirements, MIR Express streamlines data collection, minimizes errors, and maximizes compliance.

By incorporating MIR Express into your reporting workflow, your company can minimize exposure to civil money penalties (CMPs) and streamline claims reporting. Enjoy peace of mind knowing that your reports are pre-validated, ensuring accuracy and compliance. With efficient reporting, your administrative teams gain valuable time to focus on other critical processes.

Request a demo today and unlock the power of seamless, compliant reporting with MIR Express.

In the complex realm of insurance, claims processing is crucial in managing risks and providing timely resolutions. However, traditional methods are often plagued by inefficiencies and limited insights. That’s where data analytics comes in.

Data analytics in claims processing revolutionizes the landscape, enabling self-insured entities to prevent and mitigate losses efficiently. Organizations can enhance operational effectiveness, streamline workflows and make informed decisions by harnessing the power of claim processing data analytics.

In this blog, we will explore the transformative role of data analytics in claims management and processing and the benefits it brings to self-insured entities. These data analytics capabilites were only available to large organizations in the past, but new tools make them available to all.

Understanding Data Analytics in Claims Processing

In claims processing, data analytics has emerged as a transformative force. But what exactly is data analytics, and how does it apply to claims management?

Data analytics involves systematically analyzing large volumes of data to extract meaningful insights, patterns and trends. In claims processing, it entails leveraging sophisticated algorithms and tools to process incident-related data, claim-related data, including policy information, loss data and customer details.

Data analytics in claims management plays a crucial role in uncovering valuable insights and optimizing the entire claims process. By analyzing vast amounts of data, self-insured entities can identify trends, patterns and anomalies that help in risk assessment and operational efficiency. This allows these organizations to make informed decisions, enhance customer satisfaction and mitigate losses effectively.

Benefits of Data Analytics in Claims Processing

Data analytics plays a pivotal role in revolutionizing claims processing for self-insured entities. By utilizing data analytics in claims management, significant benefits can be achieved.

1. Enhanced Risk Mitigation

One significant benefit of data analytics in claims management and processing is that it empowers self-insured entities to identify and mitigate risks effectively. Organizations gain valuable insights that enable proactive risk management by analyzing patterns and trends in incident and claims data.

For example, identifying frequent causes of incidents, claims or high-risk areas allows entities to implement targeted risk mitigation strategies that may include training and policy updates. They can also analyze historical data to identify emerging risks and take preemptive measures. Leveraging data analytics in claims management provides a comprehensive understanding of risks, enabling self-insured entities to make informed decisions and allocate resources strategically.

This proactive approach enhances risk mitigation efforts, reduces potential losses and fosters a culture of proactive risk management within the organization.

2. Improved Cost Control

Data analytics in claims processing offers substantial cost-saving potential for self-insured entities. By leveraging data analytics, they can identify cost drivers and optimization opportunities within their claims management process. Analyzing claim data allows for a granular understanding of where costs are incurred and where efficiencies can be gained.

With data-driven insights, entities can make informed decisions for better cost control and financial stability. By optimizing processes, reducing wasteful spending and allocating resources effectively, self-insured entities can maximize cost savings.

Embracing data analytics in claims management empowers organizations to achieve financial efficiency and long-term sustainability.

3. Expedited Claims Processing

Carriers can reduce manual effort and save valuable time by leveraging data analytics tools and technologies. Automation streamlines routine tasks, such as data entry, document verification and claim assessment, allowing faster and more efficient processing.

Expedited claims processing can lead to quicker resolutions and improve customer satisfaction. Policyholders receive prompt responses and settlements, enhancing their overall experience. By leveraging data analytics in claims management, organizations can achieve operational efficiency and deliver swift, hassle-free claim services to their policyholders.

4. Improved Decision-Making

Data analytics in claims processing empowers self-insured entities to make informed and strategic decisions. Organizations can gain a comprehensive understanding of claims management, reserves and risk mitigation strategies.

For instance, analyzing historical data helps identify trends, patterns and correlations that can help inform decision-making. Self-insured entities can accurately assess claim severity, allocate reserves effectively and implement targeted risk mitigation strategies based on data analytics. These insights enable organizations to optimize resource allocation, streamline processes and make proactive decisions that align with their objectives.

5. Stakeholder-Centric Approach

Utilizing data analytics in claims processing can empower entities to deliver a stakeholder-centric claims experience, where stakeholder can range from employees, to customers and vendors. Organizations can personalize their claim services and tailor solutions based on stakeholder data.

Analyzing stakeholder behavior, preferences and past interactions allows customized communication, proactive outreach and tailored claims-handling processes. This stakeholder-centric approach enhances the overall claims experience, improves stakeholder satisfaction and fosters loyalty. By leveraging data analytics in claims management, you can understand your stakeholders better, anticipate their needs and provide timely and relevant support.

This focus on the stakeholder strengthens relationships, boosts retention and establishes a reputation for exceptional service.

6. Continuous Improvement

Organizations can identify areas for improvement and drive ongoing operational excellence by tracking key performance indicators (KPIs) and leveraging data insights. Data analytics provides valuable metrics and trends that enable self-insured entities to measure performance, identify bottlenecks and streamline processes.

Organizations can continuously analyze data to implement targeted enhancements, optimize workflows and improve efficiency. This iterative approach to leveraging data analytics in claims management ensures that self-insured entities stay proactive and responsive to changing needs, driving continuous improvement and maximizing their outcomes.

7. Enhanced Reporting and Insights

Data analytics in claims processing can empower self-insured entities to generate comprehensive reports and gain valuable insights. Leveraging advanced tools and techniques allows organizations to transform complex claims data into intuitive visualizations — enabling a better understanding of trends, patterns and outliers.

Enhanced reporting and insights provide a clear overview of claims performance, reserve analysis and risk exposure. These actionable insights support strategic decision-making, enabling organizations to identify areas for improvement, optimize resource allocation and ensure regulatory compliance. With data analytics in claims management software, self-insured entities can harness the power of data visualization to drive informed decisions and achieve operational excellence.

The Future of Claims Processing and Data Analytics

The future of claims processing is closely intertwined with the rapid advancements in data analytics. As self-insured entities strive for more efficient and effective claims management, emerging trends in data analytics are set to revolutionize the industry. One such trend is the integration of artificial intelligence (AI) and machine learning (ML) technologies into claim management systems.

These technologies can automate manual processes, analyze vast amounts of data in real-time and provide accurate predictions and insights. AI-powered algorithms can quickly identify patterns and anomalies, improving fraud detection and risk mitigation.

Additionally, predictive analytics can help anticipate claim outcomes, enabling proactive decision-making. The continuous evolution of data analytics in claims management software ensures that self-insured entities can leverage the power of data to enhance operational efficiency, drive cost savings and deliver exceptional customer experiences.

As the industry evolves, data analytics will remain a vital tool in shaping the future of claims processing, enabling self-insured entities to stay ahead of the curve.

Revolutionize Your Claims Processing With Cloud Claims by APP Tech

To summarize, data analytics in claims processing is the driving force behind the insurance industry’s transformation. By harnessing the power of data, self-insured entities can prevent and mitigate loss, streamline operations and improve customer satisfaction.

To unlock these advantages, we introduce Cloud Claims, an incident-based, claims-focused risk management information system (RMIS) by APP Tech. Experience the benefits of Cloud Claims, including expedited claims processing, time savings, greater oversight, enhanced risk mitigation, complete customization and user-friendly reporting capabilities. With its cloud-based accessibility, all stakeholders can access the platform, receive alerts and ensure regulatory compliance.

Take the next step toward optimizing your claims management process by contacting APP Tech to learn more about Cloud Claims and how it can benefit your organization.

Digital Modernization of Claims Management

In the ever-evolving landscape of insurance, claims management stands as a critical function for self-insured entities, third-party administrators (TPAs) and insurance solution providers. Claim management involves the efficient handling of claims, ensuring timely resolution and mitigating financial risks.

However, with the increasing complexity and diverse portfolios, traditional systems fall short of meeting the demands of today’s digital age. Additionally, as the next generation workforce drives the digital transformation in the insurance consumer industry, the next generation of claim managers expect access to similar streamlined solutions in the workplace.

Enter the role of advanced technology in claims management — a catalyst for streamlined operations, improved customer experiences and cost savings. Leveraging digital transformation, technology revolutionizes the way claims are processed, analyzed and handled.

At the heart of this revolution lies claim management software and advanced claims management systems, empowering its users to simplify and expedite the processing of claims. By automating workflows, integrating with data in existing systems and enabling real-time analytics, technology elevates claims management to new heights.

In this blog, we delve into the pivotal role of technology in claims management, exploring how it reshapes the industry and the benefits it brings.

Traditional Claims Management

Before the advent of technology in claims management, manual processes presented some significant challenges and limitations. These conventional methods hindered efficiency and left room for errors and delays. The following are key drawbacks of traditional claims management that have necessitated the rise of technology in claims management:

- Time-consuming processes: Manual claims management involves time-consuming processes and excessive paperwork. Handling and processing claims manually led to repetitive tasks, data entry and document management — consuming valuable time and resources.

- Inefficiencies and potential errors: Inefficiencies were rampant in traditional claims management, particularly when relying on tools like spreadsheets. These methods lacked automation and validation mechanisms, making them prone to errors and inconsistencies. The complexity of claims portfolios often overwhelmed manual systems, leading to inefficiencies and delays in processing.

- Lack of real-time data and analytics: Traditional methods needed help to provide real-time data and analytics. Access to timely and accurate information is necessary for decision-making to become easier. In contrast to modern claim management software, traditional approaches relied on outdated data and lacked robust analytics capabilities.

- Inefficient communication and collaboration: The reliance on emails and manual coordination slowed down processes, impeding the flow of information between stakeholders. Assigning critical tasks to users only works if done infrequently, otherwise tasks can be forgotten or fail to be reassigned before deadlines are missed.

That said, there are some other common challenges in claim management today that technology-driven solutions can resolve.

The Role of Technology in Claims Management

Technology has revolutionized claims management, empowering those in the claims industry to overcome traditional challenges and enhance operational efficiency. Several technologies have emerged as game-changers in the realm of claims processing:

Claim Management Software

Claim management software platforms are at the forefront of the technological transformation in claims management. These platforms offer a range of features and benefits, which may include:

- Customizable workflows and automation: A claims management system may allow the creation of tailored workflows, automating manual tasks and eliminating redundant processes. This system streamlines claim handling, accelerates decision-making and improves overall efficiency.

- Centralized data management and integration: Modern systems provide a centralized repository for claim-related data, ensuring seamless integration with various data sources. They eliminate data silos, enhance data accuracy and facilitate comprehensive analysis for better decision-making.

- Real-time visibility and reporting: Some claim management software offers real-time visibility into the status of claims, enabling stakeholders to monitor progress, identify bottlenecks and take timely actions. Advanced reporting capabilities provide actionable insights, performance metrics and compliance tracking.

Robotic Process Automation (RPA)

An RPA is another technology transforming claims management. RPA utilizes software robots to automate repetitive and rule-based tasks. In claims management, RPA can perform tasks such as data entry, document extraction and verification, reducing human errors and accelerating claim processing.

Artificial Intelligence (AI)

AI technologies, including machine learning and natural language processing (NLP), have a profound impact on claims management. AI-powered algorithms can analyze vast amounts of structured and unstructured data to identify patterns and predict future trends. AI-driven chatbots and virtual assistants also enhance customer interactions, providing quick responses and personalized support.

Big Data

The exponential growth of data in the digital age has led to the emergence of big data analytics in claims management. By harnessing large volumes of structured and unstructured data, insurers can gain valuable insights into claims trends, risk assessment and pricing models. Big data analytics enables proactive decision-making and predictive modeling for better claims management outcomes.

The role of technology in claims management is multi-faceted, offering streamlined workflows, centralized data management, real-time visibility, automation, AI-driven intelligence and big data analytics.

The Benefits of Modernizing Technology in Claims Processing

In the ever-evolving landscape of claims management, technology continues to play a pivotal role, driving significant advancements and delivering a wide array of benefits. Let us explore the future of technology in claims management and how it simplifies and expedites the ingestion of claim data and enhances overall efficiency.

1. Streamlined Processes and Improved Efficiency

Technology-driven claim management software and systems revolutionize the way claims are processed. By automating manual tasks and providing an intuitive user interface, technology expedites claim processing. Users can easily input claim data, including pictures taken in the field, to accelerate the entire process. Key events and tasks are promptly alerted, ensuring timely actions and preventing delays.

2. Enhanced Data Management and Analysis

Technology empowers claims professionals with robust data management and analysis capabilities. Claims management systems efficiently capture and store data, allowing for easy retrieval and analysis. Risk managers can leverage comprehensive reporting data to identify future trends, patterns and potential risks. This data-driven approach helps mitigate risks effectively and make informed decisions.

3. Improved Client Satisfaction and Service Delivery

By leveraging technology, claims management processes become more client-centric, resulting in improved client satisfaction and service delivery. Technology-enabled platforms provide users with self-service options, granting them quick access to claim information and status updates. This transparency enhances communication and collaboration between claims professionals and clients, fostering stronger relationships.

Embrace the future of technology in claims management to simplify and expedite your operations. Invest in cutting-edge claim management software and systems that enable efficient claim data ingestion, streamlined processing and robust reporting capabilities.

The Future of Technology in Claims Management

As we look into the future of technology in claims management, the possibilities are vast. Insurtech continues to evolve, presenting new opportunities to enhance the claims process and customer journey.

We can anticipate exciting advancements in AI, estimating software and other technologies that will further streamline operations and improve the overall claims experience. Embracing these innovations will empower those in insurance and risk management to stay ahead of the curve, delivering efficient and customer-centric claims management.

Elevate Your Claims Management With Cloud Claims by APP Tech

Discover the transformative power of technology in claims management with Cloud Claims, an incident-based, claims-focused risk management information system (RMIS) by APP Tech. This innovative solution empowers self-insured entities, TPAs and insurance providers to streamline and expedite claims processing.

Cloud Claims’ incident-based design enables companies to log any incident, even without associated claims, providing valuable risk management insights. By identifying patterns and mitigating risks, self-insured companies can cut claims costs and enhance overall risk management strategies.

Experience the benefits of Cloud Claims, including streamlined claims processing, prevention of data duplication, time savings, greater oversight, complete customization and user-friendly reporting capabilities. With its cloud-based accessibility, all stakeholders can access the platform, receive alerts and ensure regulatory compliance.

Learn more about Cloud Claims today to elevate your claims management practices. Contact APP Tech for more information about this user-friendly and secure claims management solution. Unleash the full potential of technology in claims management and drive efficiency in your operations.

As businesses face growing risks and potential losses, effective claims processing is crucial for managing and mitigating those risks. However, traditional claims processing methods often focus on managing claims after they occur rather than preventing them from happening. An incident-based approach to claims processing can help businesses identify and address potential risks before they escalate into full-blown claims.

Basics and Components of Risk Management in Claims Processing

Risk management in claims processing involves identifying, assessing and mitigating potential risks that could lead to claims against a business. It is a crucial component of claims processing and helps businesses minimize losses and protect their assets. The basics and components of risk management in claims processing include:

- Risk identification: This involves identifying all the potential risks that could lead to claims against a business. These risks can be internal, such as employee errors, or external, such as non-preventable vehicle accidents or customer injury.

- Risk assessment: After identifying potential risks, the next step is to assess the likelihood and impact of those risks. This helps businesses prioritize risks and determine which ones require the most attention.

- Risk mitigation: When a potential risk has been identified and assessed, businesses can develop strategies to mitigate it. This can include implementing safety procedures, improving employee training or investing in insurance coverage.

- Risk monitoring and review: Risk management is an ongoing process, and it is essential to continuously monitor and review risks to ensure that risk mitigation strategies are effective. This can involve regular audits, employee feedback or reviews of insurance coverage.

- Claims handling procedures: It is essential to have effective claims handling procedures in place, including clear guidelines for reporting and investigating claims, as well as a plan for managing claims once they occur.

- Communication and reporting: Effective communication is critical to successful risk management in claims processing. Businesses should establish clear lines of communication between employees, management and insurance providers and ensure that all stakeholders are informed of any potential risks or claims.

Overview of Risk Management Information Systems

A risk management information system (RMIS) is a software tool that helps businesses manage and analyze risk-related data. It provides a centralized platform for storing, organizing and analyzing risk data, enabling businesses to make informed decisions and reduce the likelihood of losses due to risks.

An RMIS typically includes several components, such as:

- Data collection and storage: An RMIS collects and stores data related to risk management, including incident reports, incident photos, insurance policies, claims data and other relevant information.

- Risk assessment: An RMIS enables businesses to assess and analyze potential risks by analyzing data and identifying patterns and trends.

- Claims management: An RMIS provides tools for managing claims, including claims reporting, tracking and settlement processes.

- Reporting and analytics: An RMIS provides reports and analytics to help businesses understand their risk exposure and make informed decisions about risk management strategies.

Reasons to Have a Fully Integrated Risk and Claims Management System

There are several reasons businesses should consider implementing a fully integrated risk and claims management system. Some of these reasons include:

- Improved efficiency: Integrating risk and claims management systems can help businesses streamline processes and reduce duplication of effort. By having a single system that handles both risk and claims management, businesses can eliminate the need for multiple systems and processes, reducing the time and resources required for managing risk and claims.

- Enhanced data analysis: By integrating risk and claims management systems, businesses can analyze data from both systems together, enabling them to identify patterns and trends that may not be apparent when analyzing each system separately. This can help businesses make more informed decisions about risk management strategies and improve overall risk posture.

- Better risk mitigation: An integrated risk and claims management system can help businesses identify potential risks and implement strategies to mitigate them more effectively. By having a comprehensive view of all the risks faced by the organization, businesses can develop more targeted risk mitigation strategies that address specific areas of concern.

- Improved claims management: By integrating risk and claims management systems, businesses can improve their claims management processes. They can track claims more effectively, automate the claims handling process and reduce the time and resources required for claims management.

- Better communication and collaboration: An integrated risk and claims management system can improve communication and collaboration between different departments and stakeholders involved in risk and claims management. This can help ensure everyone is on the same page and that risks and claims are managed effectively.

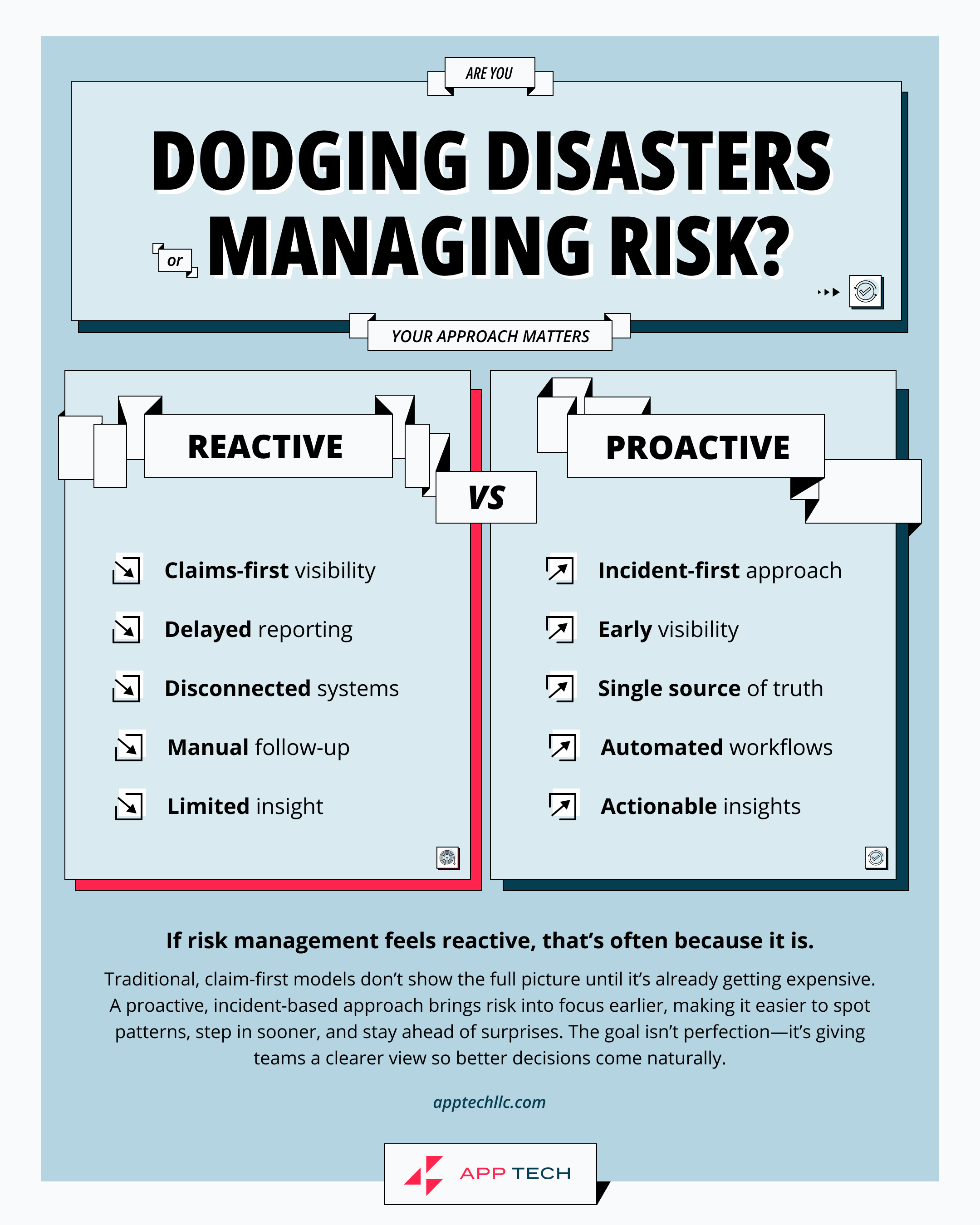

Incident-Based Approaches to Claims Processing

An incident-based approach to claims processing rejects the traditional workflow of working with each individual claim. Instead, you track any incident where a claim may or may not arise. This approach offers key benefits:

- Risk mitigation: Incident-based approaches empower self-insured businesses to identify risks and create systems for preventing them. For example, if injuries or near-injuries continue to happen on the same machine, training and operational procedures need to change. Businesses can also use incidents to find opportunities for early intervention and prevent claims from being submitted.

- Reporting consolidation: Streamline claims management by generating multiple claims from a single incident. For example, a multi-car accident may involve several medical and auto claims. Pull all relevant details from the incident to prevent redundancy and ensure consistency across all claims.

- Insight: Collecting incident data informs your business about the most prevalent incidents and drives decision-making. Incident-related decisions may involve changes to policies or instructions for employees to reduce liability. With improved oversight, you can gauge the value of these changes over time and justify the value of investments when required.

Trust Cloud Claims for an Incident-Based Approach to Claims Management

Effective claims processing is critical for managing and mitigating risks, but traditional methods may not be enough to prevent future claims. An incident-based approach to claims processing can help businesses identify and address potential risks before they escalate into claims. By encouraging incident reporting, investigating incidents, mitigating risks and continuously improving, businesses can create a safer work environment, save money and enhance their reputation.

Cloud Claims is a powerful and user-friendly cloud-based risk and claims management system, unlike other claims management solutions on the market. By leveraging the modern concept of incident-based reporting, Cloud Claims is a single platform for risk management and claims processing. Key features include:

- Easy incident reporting: Cloud Claims lets businesses report incidents quickly and easily, reducing the time and effort required to submit incident reports. The system provides customizable forms and fields, making it easy to capture all relevant information related to the incident.

- Automated claims management: Cloud Claims automates the claims management process, from initial reporting to final settlement. This can help businesses reduce the time and resources required for claims management and ensure that claims are processed efficiently.

- Comprehensive data analysis: Cloud Claims provides comprehensive data analysis capabilities, allowing businesses to identify trends and patterns related to incidents and claims. Analyze data within the platform or export to your preferred business intelligence engine. This can help businesses make more informed decisions about risk management strategies and improve overall risk posture.

- Real-time collaboration: Cloud Claims provides real-time collaboration capabilities, enabling all stakeholders to work together seamlessly. This collaboration can be particularly valuable for businesses with third-party administrators and large enterprises with several locations.

- Scalability: Cloud Claims is highly scalable, making it suitable for businesses of all sizes. Whether you have a small business or a large enterprise, the system can be customized to meet your specific needs.

With its user-friendly interface, comprehensive data analysis capabilities and real-time collaboration features, Cloud Claims is an excellent choice for incident-based claims management. Contact us to schedule a demo.

Incident-based claims management software for self-insured companies, third-party administrators, and insurance providers.

Learn MoreA Medicare, Medicaid, and SCHIP Extension Act of 2007 (MMSEA) Section 111 reporting compliance solution.

Learn MoreCONTACT

At Your Service

CONTACT

At Your Service

CONTACT

At Your Service

SUPPORT

Submit A Ticket

CONTACT